DIY Will: The No-Lawyer Setup That Actually Holds Up

You can create a will without a lawyer—if you follow your state’s rules and don’t botch the signing. Here’s the practical, step-by-step DIY setup (plus the traps that make wills fall apart).

Imagine this: you get hit with a random medical emergency, and your family’s stuck playing “guess what they would’ve wanted” while juggling bills, passwords, and a whole lot of stress. Not fun. And the wild part? Most of that chaos is avoidable with a basic will.

I’m going to say the quiet part out loud: you can create a legit will without a lawyer in many situations. Not always. But often enough that it’s worth learning the playbook. And if you’re a tech-savvy person who can set up two-factor authentication without breaking a sweat… you can handle a simple will.

The Problem (and Why People Keep Avoiding It)

People skip wills for three main reasons:

- It feels morbid. (Because it kinda is.)

- They think it’s expensive. (Sometimes. Not always.)

- They think it’s complicated. (It can be, but a basic will usually isn’t.)

Meanwhile, the world keeps reminding us how fast things can go sideways. We’re watching headlines about governments cracking down, internet blackouts, and even a G4 severe geomagnetic storm that can disrupt communications and power grids.[4][7][9] I’m not saying “write a will because space weather.” I’m saying: uncertainty is normal now. Paperwork is a weirdly powerful form of preparedness.

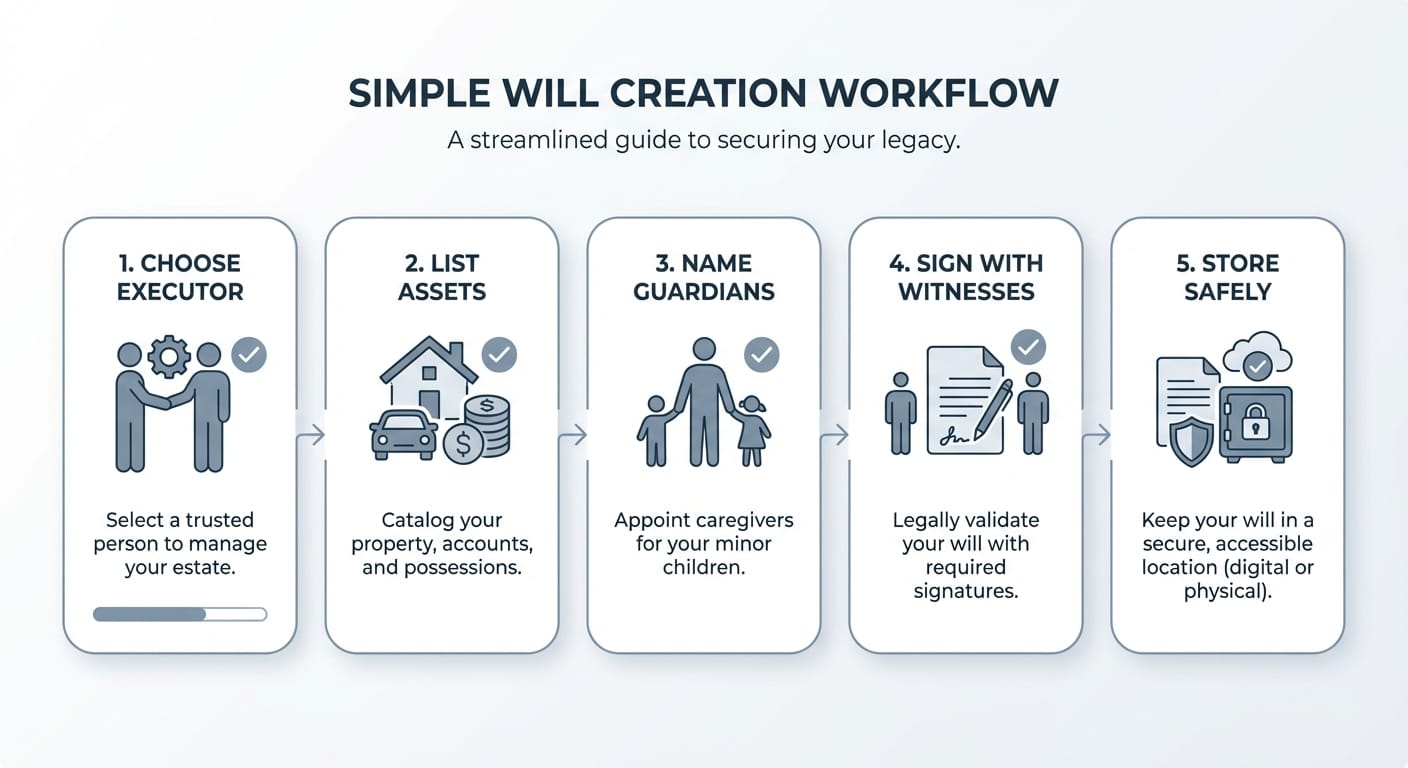

The DIY Will Plan (Step-by-Step)

This is the practical, no-fluff flow. Think of it like setting up a new laptop: gather your stuff, pick your config, hit save, and back it up.

Step 1: Confirm your state’s rules (this part matters)

Wills are state-law creatures. The basics are pretty consistent, but the details (witnesses, notarization, handwritten wills) can vary.

- Most states require two adult witnesses who watch you sign.

- Some states recognize holographic (handwritten) wills, some don’t.

- A notary often isn’t required for validity, but can help make it “self-proving” so witnesses don’t have to testify later.

Start here for state-by-state references and plain-language guidance: Nolo’s overview of state will requirements is a solid jumping-off point.[1]

Step 2: Inventory your “stuff” (assets + accounts)

If you skip this, you’ll write a will that sounds nice but doesn’t actually cover your life. Make a list:

- Home/real estate

- Cars

- Bank + brokerage accounts

- Retirement accounts (401(k), IRA)

- Life insurance

- Business ownership (LLC shares, side hustles)

- Digital assets: crypto wallets, domains, revenue-generating accounts

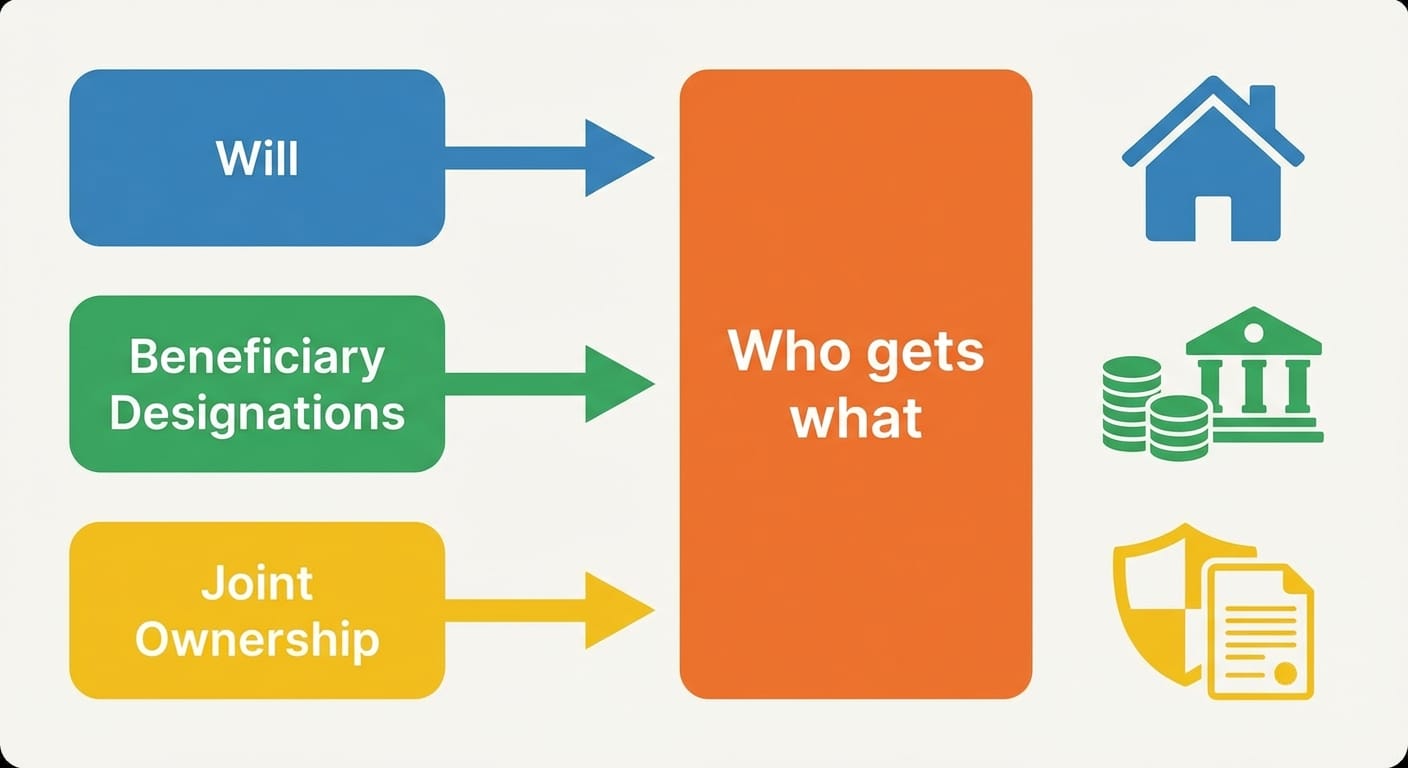

Quick reality check: a will doesn’t control everything. Beneficiary-designated assets (life insurance, many retirement accounts) usually pass outside the will.[2] So yes, your will matters—but your beneficiary settings matter too.

Step 3: Choose an executor (the “project manager” of your will)

Your executor is the person who makes the whole thing happen—filing paperwork, paying final bills, distributing assets.

Pick someone who is:

- Organized

- Trustworthy

- Not easily steamrolled by other relatives

My opinion: “Oldest child” is not an executor qualification. It’s a job, not a birthright.

Step 4: Name guardians (if you have minor kids)

If you have kids under 18, this is the headline feature. Courts ultimately decide guardianship, but a will is where you clearly state your preference.

Also: name a backup guardian. People move. People get sick. People change their minds. Your plan should survive reality.

Step 5: Write the will (simple language wins)

You’ve got three realistic options:

- Reputable online will maker (best for most DIY cases)

- Attorney-reviewed template (better if you’re comfortable editing carefully)

- Handwritten will (only if your state recognizes it—and even then, it’s riskier)

For DIY, online tools can work well, as long as they’re state-specific and walk you through witnesses properly. The FTC specifically advises consumers to be careful with “do-it-yourself” legal products and to understand what you’re buying.[3]

Step 6: Sign it correctly (where DIY wills go to die)

This is the “deploy to production” moment. Follow your state’s execution rules exactly. Typically:

- Sign in front of two witnesses (not beneficiaries, ideally)

- Witnesses sign immediately after

- Consider adding a self-proving affidavit notarized with the witnesses (if your state supports it)

If you mess up signing, it doesn’t matter how beautifully you wrote the will. A court can treat it like fan fiction.

Step 7: Store it like you actually want it found

Do not hide it so well nobody can locate it.

- Keep the original in a safe place (home safe or fireproof box works)

- Tell your executor where it is

- Keep a scanned copy for reference (but know the original is what usually matters)

The American Bar Association recommends making sure your executor knows where your documents are and keeping things accessible when needed.[5]

Common Mistakes (Don’t Do These)

- Using vague language like “I leave everything to my family.” (Which family? Who decides?)

- Forgetting contingencies (“If my spouse is not living, then…”)—because life happens.

- Picking witnesses who inherit—some states reduce or void gifts to interested witnesses.

- Thinking a will avoids probate—it usually doesn’t. It just tells probate what to do.

- Never updating it after marriage, divorce, kids, moving states, or buying a home.

Tool/Resource Recommendations (The Stuff I’d Actually Use)

- State court / state bar websites: dry, but accurate for execution rules.

- Nolo’s will guides: solid educational baseline.[1]

- FTC guidance: helpful for evaluating online legal services and avoiding sketchy upsells.[3]

- ABA consumer resources: practical “what to do next” estate planning pointers.[5]

FAQ (Because You’re Probably Wondering)

1) Is a DIY will actually legal?

Yes—if it meets your state’s legal requirements (capacity, intent, proper signing/witnessing). The signing formalities are the big one.[1]

2) Do I need a notary?

Usually not for validity, but notarization can help create a “self-proving” will so your witnesses don’t have to be tracked down later. This is state-dependent.[1]

3) What if I have a house, kids, and a small business?

You can still do DIY sometimes, but I’m more cautious here. Businesses, blended families, special needs planning, or tax concerns can turn “simple” into “lawyer territory” fast.

4) Does my will cover my 401(k) and life insurance?

Often no—those pass by beneficiary designation. That’s why you should audit beneficiaries as part of the process.[2]

Action Challenge: Do This Today (Seriously, 20 Minutes)

Open a notes app (or a spreadsheet if you’re one of my people) and write down:

- Your executor choice

- Your guardian choice (if you have kids)

- Your top 10 assets/accounts

- Where your important documents live

That’s not a will yet—but it’s the hardest part of writing one. Tomorrow, you can plug that info into a state-specific template or an online will tool and finish the job.

One last Marty take: a DIY will isn’t about being cheap. It’s about being responsible without making it a whole production. If your situation is simple, ship the will. If it’s complicated, pay a pro. Either way, don’t leave your family a scavenger hunt.

Sources: [1] Nolo, “State Requirements for Making a Will” (state-by-state overview), https://www.nolo.com/legal-encyclopedia/state-requirements-making-will-30046.html • [2] Consumer Financial Protection Bureau (CFPB), guidance on beneficiaries and account transfers (consumer resources), https://www.consumerfinance.gov/consumer-tools/retirement/ • [3] Federal Trade Commission (FTC), consumer guidance on legal services and avoiding misleading claims, https://www.ftc.gov/ • [4] NOAA Space Weather Prediction Center (SWPC), geomagnetic storm scales and alerts, https://www.swpc.noaa.gov/ • [5] American Bar Association (ABA), estate planning consumer information, https://www.americanbar.org/groups/real_property_trust_estate/resources/estate_planning/ • [7][9] Reuters / UN-reported crisis summaries in provided research dataset (Jan 20-21, 2026).